IRS APPROVED ERO SERVING ALL 50 STATES

RAPID REFUNDS - TAX REFUND LOANS - VERY LOW FEES

OVER 15 YEARS EXPERIENCE

IRS APPROVED ERO SERVING ALL 50 STATES

RAPID REFUNDS - TAX REFUND LOANS - VERY LOW FEES

OVER 15 YEARS EXPERIENCE

New for 2024

Starting in calendar year 2023, the Inflation Reduction Act reinstates the Hazardous Substance Superfund financing rate for crude oil received at U.S. refineries, and petroleum products that entered into the United States for consumption, use, or warehousing. The tax rate is the sum of the Hazardous Substance Superfund rate and the Oil Spill Liability Trust Fund financing rate. For calendar years beginning in 2024, the Hazardous Substance Superfund financing rate is adjusted for inflation. For calendar year 2024 crude oil or petroleum products entered after

Dec. 31, 2016, will have a tax rate of $0.26 cents a barrel.

Highlights of changes in Revenue Procedure 2023-34:

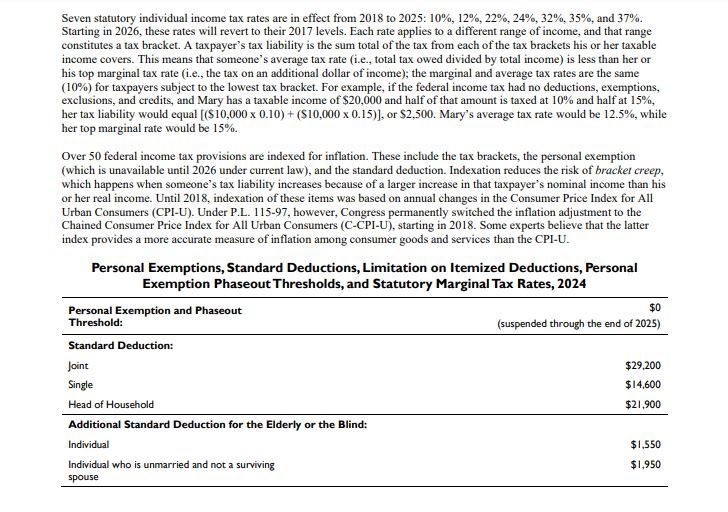

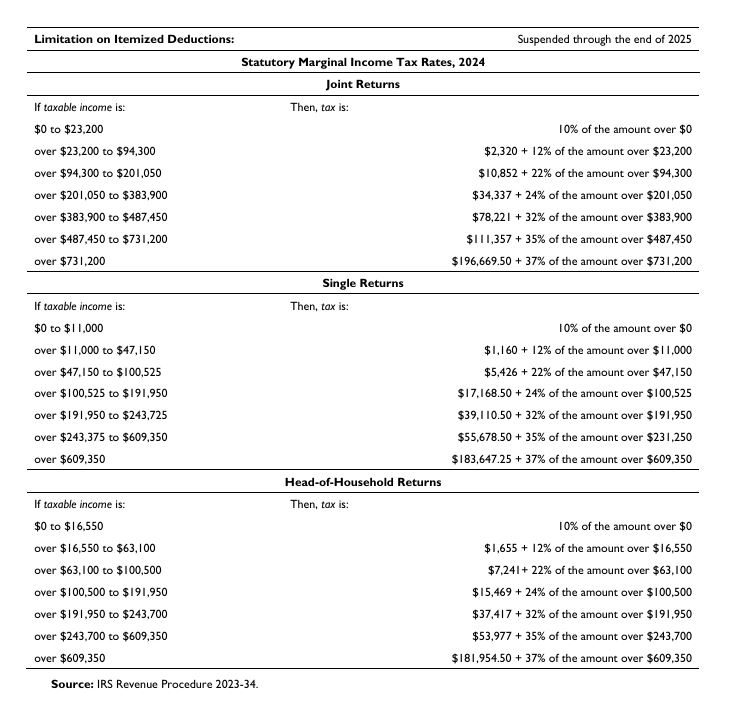

The tax year 2024 adjustments described below generally apply to income tax returns filed in 2025. The tax items for tax year 2024 of greatest interest to most taxpayers include the following dollar amounts:

The other rates are:

35% for incomes over $243,725 ($487,450 for married couples filing jointly)

32% for incomes over $191,950 ($383,900 for married couples filing jointly)

24% for incomes over $100,525 ($201,050 for married couples filing jointly)

22% for incomes over $47,150 ($94,300 for married couples filing jointly)

12% for incomes over $11,600 ($23,200 for married couples filing jointly)

The lowest rate is 10% for incomes of single individuals with incomes of $11,600 or less ($23,200 for married couples filing jointly).

Items unaffected by indexing

By statute, certain items that were indexed for inflation in the past are currently not adjusted.

Excess Social Security and Medicare withholding refunds

Special Social Security and Medicare tax exemption: A J-1 alien who is a nonresident alien for tax purposes and is paid wages in exchange for personal services performed within the United States is exempt from paying U.S. Social Security and Medicare taxes on such wages under Section 3121(b)(19) of the Internal Revenue Code, as long as the employment is authorized by USCIS and the services are performed to carry out the purposes for which the J-1 visa was issued to them.

J-1 aliens who become U.S. tax residents or change their visa status to other work visa types (other than F, M or Q visa) are subject to Social Security and Medicare taxes on their wages. However, if a J-1 alien is from a foreign country with which the United States has entered into a Totalization Agreement, he or she may claim an exemption from U.S. Social Security and Medicare taxes by securing a Certificate of Coverage from the social security agency of his or her home country and presenting such Certificate of Coverage to his or her employer in the United States, according to the procedures set forth in Revenue Procedures 80-56, 84-54, and Revenue Ruling 92-9. An alternate procedure is provided in these revenue procedures for an alien who is unable to secure a Certificate of Coverage from his or her home country. For more information, see Social Security/Medicare and Self-Employment Tax Liability of Foreign Students, Scholars, Teachers, Researchers, and Trainees.

What to do if the tax is withheld: If a J-1 alien falls into the category of employees who are exempt from Social Security and Medicare tax, he or she may discuss with his or her employer to stop withholding and refund amounts that were already withheld. Employees that are unable to obtain a refund from their employer may file a Claim for Refund and Request for Abatement.

See IRS for more, Information Regarding Request for Refund of Social Security Tax Erroneously Withheld on Wages Received by a Nonresident Alien on an F, J, or M Type Visa to obtain a refund.

© Copyright 2020 All rights reserved.

We need your consent to load the translations

We use a third-party service to translate the website content that may collect data about your activity. Please review the details in the privacy policy and accept the service to view the translations.